Volkswagen’s Brand Group Core posted a 38 percent jump in operating profit to 1.54 billion euros in the first quarter of 2026. That number looks great until you crack it open and find a half-billion-euro write-down from killing ID.4 production in Chattanooga stuffed inside.

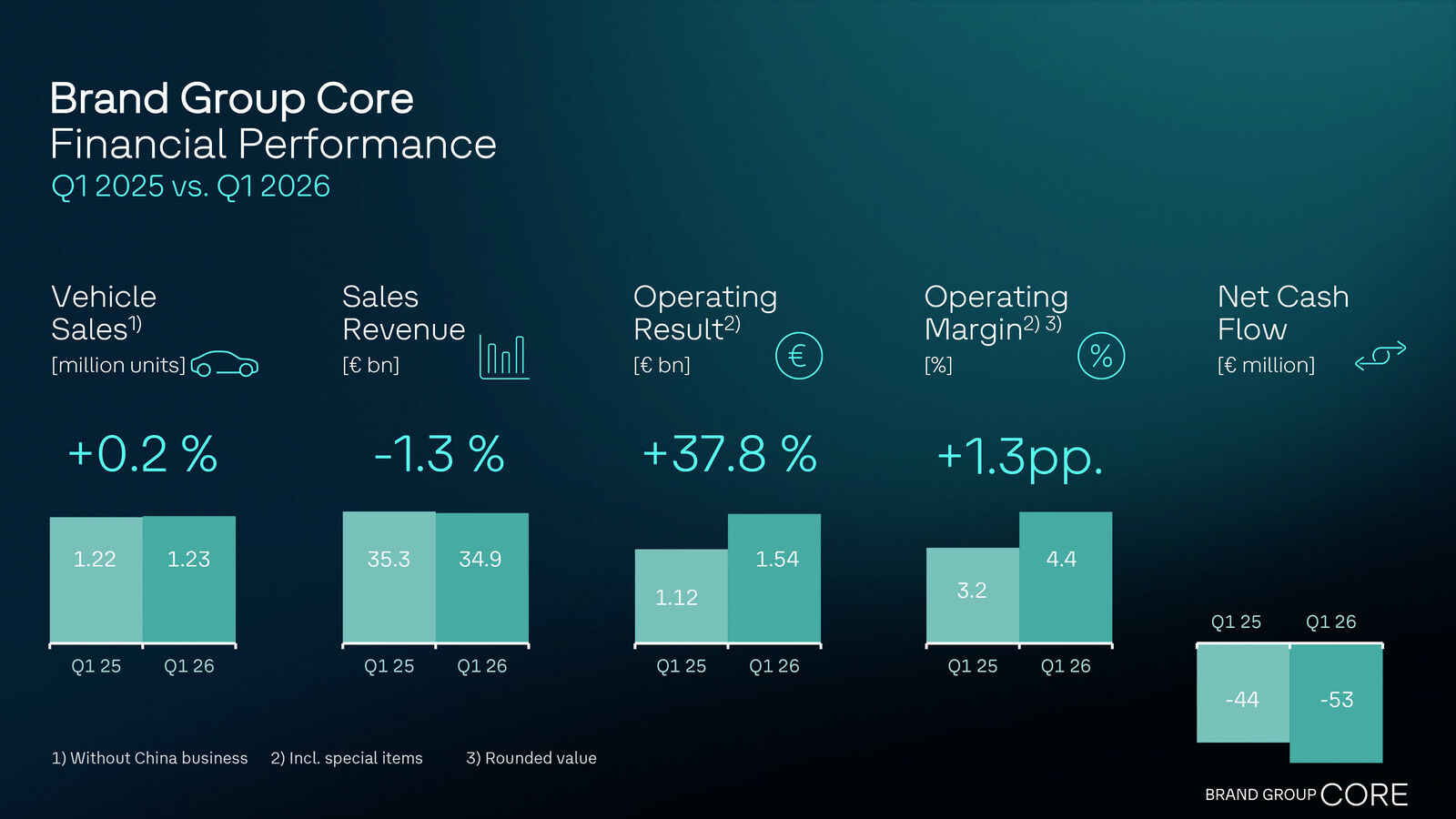

Strip out the restructuring charges and the ID.4 shutdown costs, and the group’s operating margin would have been 6.3 percent. With them, it landed at 4.4 percent. That gap tells you everything about where Volkswagen actually stands: operationally improving, strategically bleeding.

The Volkswagen passenger car brand itself scraped together a 0.4 percent operating margin. Revenue fell 6.3 percent to 19.9 billion euros. The culprits are familiar: tariff exposure in the United States, a shrinking footprint in China, and the bill for walking away from electric vehicle production in Tennessee.

Without those special items, the brand margin would have been 3.5 percent. Respectable but hardly dominant.

CFO David Powels didn’t sugarcoat it. “We are still not earning enough to sustainably finance our future,” he said. That’s a remarkable admission from the finance chief of the world’s largest volume automaker, delivered in the same quarter his group posted a significant profit increase.

The real engine of the Brand Group Core right now is Škoda. The Czech brand pushed its operating margin to 8.3 percent on strong European sales. SEAT and CUPRA climbed to 1.2 percent profitability, while Volkswagen Commercial Vehicles hit 3.9 percent. In other words, the brands that aren’t Volkswagen are doing the heavy lifting.

Chattanooga is pivoting hard. The plant will abandon the ID.4 and refocus on high-volume combustion models like the Atlas. That’s a concrete retreat from the electric push in America, driven by what VW diplomatically calls “changed market conditions.”

Translation: the U.S. EV market didn’t materialize the way Wolfsburg bet it would, and tariffs made the math even worse.

Europe is a different story. Volkswagen is about to launch the broadest electric portfolio in its history. The ID. Polo, ID. Polo GTI, ID. Cross, and ID.3 GTI are all premiering this year, joining the recently introduced ID.3 Neo.

All ride on the MEB+ platform, previously reserved for larger vehicles. The Electric Urban Car Family, four compact EVs built across VW, CUPRA, and Škoda under SEAT/CUPRA project management in Spain, is projected to unlock 650 million euros in synergies over its lifecycle.

That’s the tension at the core of Volkswagen in 2026. In Europe, it’s flooding the zone with affordable electric cars and betting on platform synergies to make the economics work. In America, it’s retreating to combustion engines and absorbing the financial damage of its pivot.

Unit sales across the Brand Group Core ticked up a marginal 0.2 percent to 1.23 million vehicles. Revenue actually declined 1.3 percent to 34.9 billion euros. Net cash flow was negative 53 million euros, roughly flat with last year’s first quarter, chalked up to seasonal working capital effects.

A new organizational restructuring took effect in January, compressing the Brand Group Board of Management to shorten decision-making and streamline overlapping structures. A fresh 2030 vision promises to slim the product portfolio, clarify responsibilities between group, brand, and regional levels, and concentrate resources where they generate competitive advantage.

Volkswagen has been promising leaner operations and faster decisions for the better part of a decade. The difference now is that the financial pressure is real, the American experiment has a price tag attached, and a Czech subsidiary is quietly outperforming the mother brand by a factor of twenty on margin. Škoda doesn’t need a 2030 vision. It’s already executing.

Share this Story